A slide-by-slide analysis of the 22+ slide pitch deck Nubank used to secure $2,000,000 in seed funding from Sequoia Capital and Kaszek Ventures in 2013.

“David Vélez founded Nubank after identifying the massive untapped potential in Latin America’s most valuable economy: Brazil. As a successful investment professional who had recruited talent for Sequoia Capital, Vélez was well-positioned to recognise opportunity, but he lacked entrepreneurial experience. After leaving his investment role, he asked himself a critical question: ‘What’s the hardest thing I can imagine myself doing?’ The answer was revolutionising the banking system in Brazil, where banking was widely hated and traditional banks dominated the market through heavy entrenchment with the state. To achieve this vision, he sought guidance in areas such as pitch deck consulting to effectively communicate his innovative ideas to potential investors.”

The founding journey proved exceptionally challenging. Rather than facing the typical startup struggle of identifying a market and product, Nubank’s core challenge was entirely different: how to rebuild the concept of a bank in a country where banking was widely despised, whilst incumbent competitors actively blocked every move. Vélez recruited co-founder Edward Wible, a Princeton-educated engineer who had been sailing in Indonesia when Vélez convinced him to abandon his own startup idea and join the mission. Wible became part of what Sequoia Capital later credited as Vélez’s ‘contrarian hires’—unconventional talent acquisitions that proved crucial to the company’s early success, despite reservations from seasoned investors.

In July 2013, Vélez raised a $2 million seed round from Sequoia Capital and Kaszek Ventures without even having co-founders formally in place at the time. Nicolas Szekasy from Kaszek famously described the investment decision: ‘It was David and his PowerPoint, and we invested in the PowerPoint.’ This remarkable vote of confidence in Vélez’s vision and presentation ability, despite minimal operational proof points, reflected the persuasive power of his pitch deck and the clarity of his strategic thinking. The investment marked a critical turning point, providing the initial capital needed to begin executing on the vision of transforming Brazilian banking.

The pitch deck successfully communicated Nubank’s core value proposition as an ‘anti-bank’ that would address the massive pain points in Brazilian banking through a consumer-centric, digital-first approach. By positioning regulation as a competitive advantage rather than a barrier, emphasising data-driven product development, and focusing initially on a single product (credit cards) in a single market (Brazil), Nubank demonstrated strategic clarity that resonated with sophisticated investors. This early success laid the foundation for explosive growth, eventually leading to Nubank becoming Latin America’s most valuable fintech company and achieving a public listing in 2021.

The opening slide immediately establishes Nubank’s grand ambition through the brand name ‘EOS – The Future of Brazilian Consumer Banking.’ This positioning choice demonstrates strategic sophistication, as it frames the company not as another fintech startup, but as the inevitable evolution of an entire industry. The subtitle creates urgency and inevitability, suggesting that consumer banking in Brazil will transform whether incumbents participate or not. By leading with ‘future’ rather than ‘alternative,’ Vélez positions investors to see themselves as early participants in a historical shift rather than backers of a risky startup experiment.

The branding choice of ‘EOS’ (later changed to Nubank) reflects the mythological Greek goddess of dawn, symbolising the beginning of a new era. This isn’t accidental positioning—it communicates that traditional banking represents the darkness before dawn, and Nubank represents the light that inevitably follows. The focus on ‘Brazilian’ rather than ‘Latin American’ demonstrates strategic focus and market understanding, acknowledging that dominating Brazil’s massive market must precede regional expansion. This geographical specificity reassures investors that the team understands the complexity of financial services regulation and won’t dilute resources across multiple markets prematurely.

What investors see: A founding team that understands the importance of narrative and positioning from day one. Rather than describing what Nubank does (digital banking), the cover communicates what Nubank represents (inevitable industry transformation). This level of strategic sophistication in presentation suggests founders who can attract top talent, create compelling customer messaging, and build a brand that transcends product features. For early-stage investors, this indicates the founders possess the vision and communication skills necessary to scale from startup to market leader.

This slide establishes the philosophical foundation that would guide Nubank’s product development, hiring decisions, and strategic priorities. The phrase ‘consumer-centric bank’ isn’t merely marketing language—it represents a fundamental architectural decision about how to build financial services. Traditional banks optimize for regulatory compliance, risk management, and profitability, often treating customer experience as a secondary consideration. Vélez’s purpose statement inverts this hierarchy, making consumer satisfaction the primary design constraint from which all other decisions flow. This philosophical clarity becomes operationally powerful when making thousands of product and policy decisions.

The specificity of ‘Brazil’ rather than generic language about ’emerging markets’ demonstrates deep market understanding and strategic focus. Brazil’s unique regulatory environment, cultural characteristics, and economic conditions require localised solutions that can’t be imported from Silicon Valley or European fintech models. By explicitly committing to build FOR Brazil rather than adapt existing solutions TO Brazil, Vélez signals that Nubank will invest in understanding local customer needs, regulatory requirements, and competitive dynamics. This specificity reassures investors that the team won’t waste resources chasing global opportunities before dominating the home market.

What investors see: A mission statement that creates clear decision-making criteria and cultural foundation for scaling. Purpose-driven companies attract better talent, create stronger customer loyalty, and maintain strategic coherence during rapid growth phases. The consumer-centric positioning also suggests a business model that can expand beyond traditional banking products into adjacent financial services, creating multiple revenue streams and defensive moats. For investors, this indicates potential for horizontal expansion and premium pricing power through superior customer experience.

[Insert image: nubank-slide-03-big-picture.webp]

The ‘anti-bank’ positioning represents one of the most sophisticated competitive framing decisions in fintech history. Rather than competing directly with incumbents on traditional banking metrics (branch locations, product breadth, regulatory relationships), Vélez redefines the competitive landscape entirely. The ‘anti’ prefix suggests that everything customers hate about traditional banking—complex fees, poor service, bureaucratic processes—will be systematically eliminated rather than incrementally improved. This positioning creates permission for radical product and operational decisions that would seem extreme if framed as ‘better banking’ rather than ‘anti-banking.’ It also generates earned media and word-of-mouth marketing by giving customers a rebellion to join rather than just a service to try.

From a strategic perspective, the anti-bank positioning creates psychological permission for customers to switch providers despite traditional banking’s high switching costs. Brazilian consumers historically maintained banking relationships for decades due to regulatory complexity, established direct deposits, and switching friction. By framing Nubank as the opposite of traditional banks rather than a competitor, Vélez reduces the perceived risk of switching—customers aren’t changing banks, they’re escaping banking altogether. This narrative reframing transforms customer acquisition from a feature-comparison exercise into an identity-alignment decision, which creates much stronger customer loyalty and higher lifetime value.

What investors see: A positioning strategy that creates sustainable competitive advantage through customer psychology rather than just operational efficiency. Anti-bank positioning suggests the potential for viral customer acquisition, premium pricing power, and defensive moats that are difficult for incumbents to replicate. Traditional banks cannot easily adopt ‘anti-bank’ messaging without undermining their existing customer relationships and regulatory positioning, creating an asymmetric competitive advantage. This indicates potential for category creation and market leadership rather than commoditized competition.

[Insert image: nubank-slide-04-current-market.webp]

This slide conducts a systematic analysis of Brazilian banking incumbents, identifying structural weaknesses that create market entry opportunities for a digital-first challenger. The research demonstrates that traditional banks have optimised for regulatory compliance and profit extraction rather than customer satisfaction, creating widespread consumer dissatisfaction despite market dominance. By quantifying customer complaints, fee structures, and service quality metrics, Vélez establishes that incumbent weaknesses aren’t temporary operational issues but fundamental strategic choices that can’t be easily corrected. This analysis provides intellectual foundation for the disruption thesis and reassures investors that market entry barriers, whilst high, aren’t insurmountable.

The competitive analysis reveals that Brazilian banks have become complacent due to regulatory protection and market concentration, creating the classic innovator’s dilemma scenario. Established players have high-cost structures, legacy technology systems, and organisational cultures that make rapid adaptation difficult. Their profitability depends on complex fee structures and high-margin products that create customer resentment but can’t be abandoned without damaging short-term financial performance. This creates a window of opportunity for a new entrant to capture market share by offering transparent pricing, superior customer experience, and modern technology infrastructure. The analysis demonstrates that disruption is possible not despite regulation, but because of how incumbents have used regulation to avoid innovation.

What investors see: A founding team that has conducted serious competitive intelligence and understands market dynamics at a granular level. The systematic analysis of incumbent weaknesses suggests that Nubank’s strategy is based on data-driven market research rather than entrepreneurial optimism. This level of competitive understanding indicates the founders can identify sustainable differentiation opportunities, predict competitive responses, and execute strategies that exploit structural advantages rather than hope incumbents won’t respond. For investors, this reduces execution risk and increases confidence in the market entry strategy.

[Insert image: nubank-slide-05-problem.webp]

The problem statement slide systematically catalogues the specific customer pain points that create market opportunity for disruption. Rather than making general claims about customer dissatisfaction, Vélez identifies concrete operational failures: excessive fees for basic services, complex bureaucratic processes, poor customer service response times, and limited digital capabilities. These aren’t abstract market inefficiencies but daily frustrations experienced by millions of Brazilian consumers who have no viable alternatives. By quantifying these problems with specific examples and customer testimonials, the slide transforms abstract market research into visceral understanding of customer needs that competitors consistently fail to address.

The strategic insight embedded in this problem analysis is that traditional banks have created these pain points not accidentally, but as inevitable consequences of their business models and regulatory relationships. High fees generate revenue, complex processes reduce operational costs, poor service maintains profit margins, and limited digital investment preserves existing infrastructure investments. This means incumbents can’t eliminate these problems without fundamentally restructuring their operations, creating sustainable competitive advantage for a new entrant designed from the beginning to solve these specific issues. The problem statement becomes the foundation for Nubank’s entire product development roadmap and go-to-market strategy.

What investors see: A comprehensive understanding of customer needs that translates into clear product requirements and competitive differentiation. The specificity of problems identified suggests the founding team has conducted extensive customer research and understands market dynamics at an operational level. This detailed problem analysis also provides a roadmap for measuring success—each pain point eliminated becomes a competitive advantage and customer acquisition driver. For investors, this indicates that product-market fit isn’t speculative but can be systematically achieved by solving well-documented customer problems.

[Insert image: nubank-slide-06-disruption-opportunity.webp]

This slide synthesises the preceding market analysis into a clear investment thesis: Brazilian banking represents a massive market with entrenched incumbents who have systematically underserved customers, creating conditions perfect for disruption. The ‘bound for disruption’ language suggests inevitability rather than possibility—transformation will happen whether investors participate or not. By presenting disruption as inevitable, Vélez frames the investment decision as choosing to be on the right side of historical change rather than betting on a risky startup hypothesis. This positioning creates urgency and reduces perceived risk by suggesting that not investing represents missing obvious opportunity rather than avoiding potential failure.

The strategic sophistication lies in connecting macroeconomic trends (Brazil’s growing middle class, increasing digital adoption, regulatory modernisation) with microeconomic customer frustrations (fees, service quality, accessibility) to demonstrate that disruption timing is optimal. Previous attempts at banking innovation in Brazil failed because market conditions weren’t aligned—regulations were too restrictive, consumer digital adoption was insufficient, or economic conditions were unstable. The slide demonstrates that these historical barriers have been systematically eliminated, creating a unique window of opportunity that justifies immediate action rather than waiting for further market development.

What investors see: A founding team that understands how to position market opportunity in terms of inevitability and timing rather than speculation and hope. The systematic buildup from competitive analysis to problem identification to disruption conclusion demonstrates analytical rigor and strategic thinking capabilities. This logical progression also provides investors with clear talking points for their own partnership meetings and due diligence processes, making the investment easier to approve internally. The ‘large industry’ emphasis signals potential for significant returns rather than niche market success.

[Insert image: nubank-slide-12-solution.webp]

The solution slide introduces Nubank’s distinctive strategic framework combining analytical rigour (‘Brain’) with emotional resonance (‘Heart’) to create sustainable competitive advantage. This isn’t marketing language but operational philosophy—every product decision, hiring choice, and customer interaction should serve both analytical optimization and emotional connection. The ‘Brain’ component encompasses data-driven product development, risk management algorithms, and operational efficiency systems that enable competitive pricing and superior service delivery. The ‘Heart’ component focuses on brand identity, customer experience design, and emotional messaging that transforms banking from a necessary evil into a source of customer pride and advocacy.

This dual approach addresses the fundamental weakness in most fintech solutions—they optimize either for analytical superiority (better rates, lower fees, more features) or emotional appeal (beautiful design, compelling marketing, brand identity) but rarely achieve excellence in both dimensions simultaneously. Traditional banks have strong analytical capabilities but terrible emotional connection; many fintech startups have strong emotional appeal but weak analytical foundations. Nubank’s solution framework explicitly commits to achieving best-in-class performance on both dimensions, creating competitive advantage that’s difficult for incumbents or new entrants to replicate because it requires excellence across completely different organisational capabilities.

What investors see: A strategic framework that creates sustainable competitive advantage through organisational design rather than just product features. The Brain-Heart approach suggests that Nubank will attract both quantitatively-oriented talent (engineers, data scientists, risk managers) and creatively-oriented talent (designers, marketers, brand strategists), creating a more complete team than typical fintech startups. This balanced approach also indicates potential for both cost leadership (through analytical optimization) and premium pricing (through emotional differentiation), maximising revenue potential and defensive moats.

[Insert image: nubank-slide-13-why-now.webp]

The ‘Why Now?’ slide addresses one of investors’ most critical concerns: market timing. Vélez identifies the specific confluence of macro shifts (Brazilian economic growth, expanding middle class, increasing financial inclusion), technology shifts (smartphone adoption, internet infrastructure, digital payment systems), and consumer behavior changes (willingness to try digital services, frustration with traditional banks) that create a unique window of opportunity. This isn’t general optimism about fintech trends but specific analysis of why 2013 represents the optimal moment to launch digital banking in Brazil. The systematic breakdown of enabling factors demonstrates that success depends on leveraging convergent trends rather than hoping for market development.

The strategic insight is that successful disruption requires multiple enabling conditions to align simultaneously—regulatory environment, technology infrastructure, consumer readiness, competitive landscape, and economic conditions. Previous attempts at Brazilian banking innovation failed because one or more of these conditions weren’t mature enough to support success. The slide demonstrates that historical barriers have been systematically eliminated: regulations have modernised, smartphone penetration has reached critical mass, consumer digital adoption has accelerated, and economic stability has improved. This convergence analysis reassures investors that success depends on execution against favorable conditions rather than hoping market conditions will improve.

What investors see: A founding team that understands market timing is crucial for startup success and has conducted systematic analysis to identify optimal entry conditions. The specific identification of convergent trends suggests that Nubank’s strategy is based on data-driven market analysis rather than entrepreneurial enthusiasm. This timing analysis also creates urgency—if conditions are optimal now, waiting longer risks allowing competitors to capture first-mover advantages. For investors, this reduces timing risk and increases confidence that market entry strategy is based on analytical insight rather than speculation.

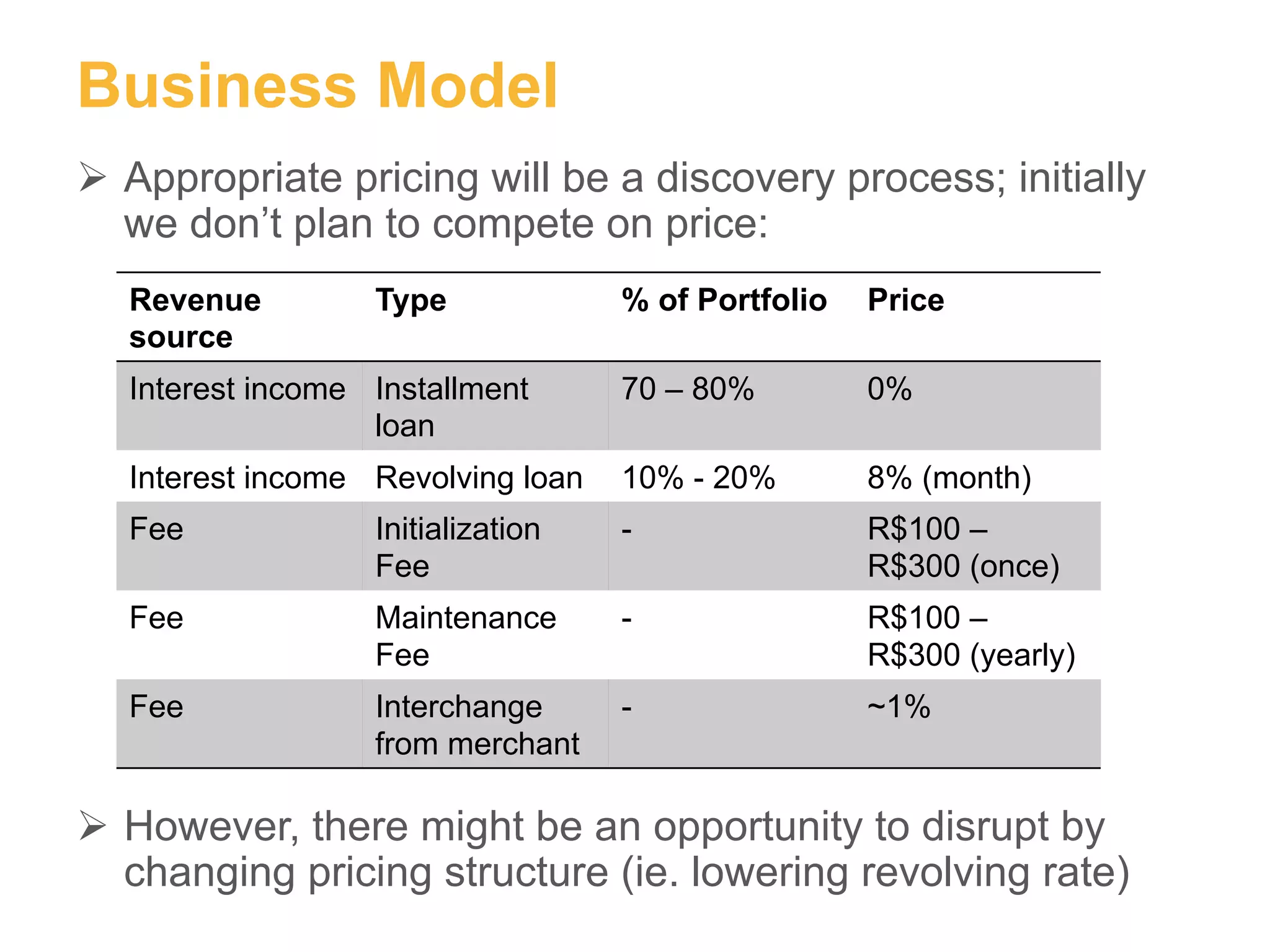

[Insert image: nubank-slide-22-business-model.webp]

The business model slide provides detailed revenue structure showing how Nubank will generate sustainable profitability while maintaining competitive pricing. Interest income comprises 70-80% of revenue from installment loans (offered at 0% to attract customers) and 10-20% from revolving loans (priced at 8% monthly, competitive with Brazilian market rates). Fee revenue includes initialization fees (R$100-300), annual maintenance fees (R$100-300), and interchange revenue (~1% from merchant transactions). This diversified revenue structure creates multiple monetisation pathways whilst allowing Nubank to offer competitive pricing on customer-acquisition products. The specific percentages and pricing demonstrate sophisticated understanding of Brazilian banking economics and customer price sensitivity.

The strategic sophistication lies in using 0% installment loans as customer acquisition tools whilst generating profit from revolving balances and fee income. This approach inverts traditional banking logic—instead of maximizing revenue per transaction, Nubank optimizes for customer lifetime value by creating initial value that encourages long-term engagement. The model also demonstrates understanding of Brazilian consumer behavior: customers value transparent, predictable pricing more than absolute lowest cost, enabling fee-based revenue generation alongside competitive interest rates. This pricing strategy creates both customer acquisition advantages and sustainable unit economics, addressing investor concerns about growth versus profitability trade-offs.

What investors see: A business model that demonstrates path to profitability whilst maintaining competitive customer acquisition costs and pricing. The detailed revenue breakdown shows the founding team understands banking economics at a granular level and has developed sustainable competitive advantage through superior cost structure and pricing strategy. The diversified revenue streams also indicate potential for expansion into additional financial products and services, creating multiple growth pathways and reducing single-product risk. This financial sophistication reduces execution risk and increases confidence in long-term viability.

While this deck secured one of the most consequential seed investments in fintech history—transforming a $2 million bet into a $30+ billion public company—it reflects the fundraising standards and investor expectations of 2013 rather than today’s more rigorous due diligence environment. Modern investors expect significantly more operational detail, financial rigor, and risk analysis than was typical during the early stages of the global fintech boom. The following elements, whilst not strictly necessary for Nubank’s successful raise, represent gaps that contemporary founders should address to meet current institutional investor standards.

While the deck outlines the business model with revenue percentages, it lacks detailed financial projections showing customer acquisition cost (CAC), lifetime value (LTV), burn rate, and path to profitability. Modern pitch decks should include 3-5 year financial forecasts with clearly stated assumptions and sensitivity analysis to demonstrate financial viability.

The deck identifies the target market (young, tech-savvy consumers in Brazil) but provides limited detail on specific customer acquisition channels, marketing strategies, partnerships, or the step-by-step execution plan. Modern decks should specify how the company will reach customers, conversion funnels, and early traction metrics.

While positioning as an ‘anti-bank,’ the deck lacks a formal competitive landscape analysis comparing Nubank to other fintech startups, traditional banks, and emerging competitors. A detailed competitive matrix would clarify Nubank’s specific competitive advantages and potential threats, which is essential for investor conviction.

The deck does not address major risks facing the business such as regulatory challenges, competitive responses from incumbents, technology infrastructure risks, or key person dependency. Modern pitch decks should explicitly identify 3-5 major risks and explain how the company plans to mitigate them.

Although the deck mentions the team, it lacks comprehensive biographical information, relevant experience, previous startup success, and complementary skill sets of founding team members and early hires. Investors heavily weight team quality, so detailed credentials and organisational structure should be clearly presented.

The deck doesn’t clearly outline the product development roadmap beyond credit cards, nor does it articulate the longer-term vision for expansion to additional products (checking accounts, savings, investments) or geographic expansion across Latin America. A clear product roadmap demonstrates strategic foresight and execution planning.

The seed-stage pitch likely lacked early user adoption data, but modern decks should include any available proof of concept, beta testing results, letters of intent, or early customer feedback demonstrating market validation. Even small traction metrics significantly strengthen investor confidence.

While the deck specifies the total funding sought, it lacks a detailed allocation of how the $2 million would be deployed across product development, team expansion, regulatory compliance, technology infrastructure, and marketing. Clear use-of-funds transparency helps investors understand capital efficiency.

These missing elements reflect the evolution of investor sophistication and market maturity since 2013, when fintech was nascent and regulatory frameworks were less defined. Today’s founders must address these components comprehensively to secure institutional funding, as investors now have extensive data on fintech unit economics, regulatory challenges, and competitive dynamics. At Projects RH, we help founders develop these critical elements systematically, ensuring their pitch decks meet contemporary investor expectations whilst maintaining the narrative clarity and strategic insight that made Nubank’s original presentation so compelling.

Nubank’s seed funding success hinged on David Vélez’s credibility, intelligence, and clarity of vision rather than operational proof points. Investors ‘invested in the PowerPoint’ because they believed in Vélez’s ability to execute. Founders should build personal credibility through track record, expertise, and network before seeking institutional capital. The lesson: strong founder credentials and demonstrated market understanding can overcome lack of early traction.

Nubank’s pitch deck powerfully positioned banking as ‘widely hated’ in Brazil, a massive economy with entrenched, inefficient incumbents. By identifying a pain point affecting millions of consumers in a large addressable market, Nubank made the opportunity obviously valuable. Founders should focus on problems affecting tens of millions of customers in multi-billion dollar markets, not niche segments.

Rather than fighting regulatory systems, Nubank explicitly decided to be ‘the kid in the front row getting A+ grades.’ This strategic positioning transformed potential adversaries into allies and created barriers to entry that competitors couldn’t easily overcome. Founders in regulated industries should reframe compliance as a defensive moat rather than a cost centre.

Although Nubank’s ultimate vision encompassed reinventing banking globally, the pitch deck concentrated on a single, laser-focused product (credit cards) in a single market (Brazil). This focused approach allowed Nubank to build deep expertise, dominate a specific customer segment, and establish proof of concept before expanding. Founders should resist the urge to pursue multiple products or geographies simultaneously.

Vélez’s ‘contrarian hires’—recruiting people without traditional startup experience or those who would typically command higher salaries—proved crucial to Nubank’s early success. By finding talented individuals willing to take big risks for meaningful ownership and impact, rather than just hiring seasoned veterans seeking job security, Vélez assembled a deeply committed founding team. This lesson suggests that founder-level conviction and mission alignment often matter more than traditional credentials.

Nubank’s deck explicitly incorporated both analytical backbone (‘Brain’) and emotional appeal (‘Heart’). By framing banking as a deeply personal, frustrating problem affecting millions of Brazilians, the pitch created emotional resonance alongside logical business fundamentals. Successful pitch decks should combine compelling narratives with data to move investors emotionally whilst maintaining analytical rigour.

The ‘Why Now?’ slide articulated a specific confluence of macro shifts, technology shifts, and consumer behaviour changes that created a unique window of opportunity. Rather than assuming market readiness was obvious, Nubank explicitly demonstrated why the timing was right. Founders should clearly articulate what specific market conditions have shifted to make success possible now, not five years ago or five years from now.

The distance between the Nubank that presented this deck and the Nubank that exists today is one of the most remarkable growth stories in global fintech history. When David Vélez pitched to Sequoia Capital and Kaszek Ventures in July 2013, Nubank was three founders with a PowerPoint presentation and a $2 million seed round. Today, Nubank is Latin America’s most valuable fintech company, a publicly-traded entity with over $30 billion in market capitalisation, serving more than 70 million customers across multiple Latin American markets with thousands of employees and billions in annual revenue.

From an investor perspective, Nubank represents one of the most successful venture capital investments in Latin American history. Sequoia Capital and Kaszek Ventures’ $2 million seed investment in 2013 has generated returns exceeding 15,000x based on the company’s public market valuation, representing the kind of transformational outcome that defines venture capital success. The investment thesis—that Brazilian banking was ripe for disruption by a consumer-centric digital challenger—proved not just correct but dramatically understated the market opportunity and Nubank’s execution capabilities.

The broader lesson for investors and founders is that exceptional pitch decks don’t just communicate business opportunities—they identify and articulate transformational market shifts before they become obvious to the broader market. Vélez’s ability to see the convergence of regulatory modernisation, consumer digital adoption, and incumbent complacency in Brazilian banking, combined with his team’s execution excellence, created one of the most successful fintech companies globally. This demonstrates that the most valuable investments often come from backing founders who can clearly articulate why massive, established markets are about to change fundamentally.

At Projects RH, we help companies across all industries create investor-ready materials that close deals. Our integrated capital raising package ensures consistency across all your investor documentation.

Built in-house for accuracy and investor confidence.

Comprehensive investor documentation following global best practices.

12-slide investor-ready presentation with supporting materials.

High-impact snapshot to capture investor attention fast.

Browse our collection of real pitch deck breakdowns from the world’s most successful companies.

Based on the search results, Nubank's seed-stage pitch deck contained 22 or more slides. The documented slides include the cover, purpose statement, market analysis, problem statement, solution, why now, business model, and other supporting materials. The exact total is difficult to determine from available sources, but the deck was comprehensive enough to cover all major business plan components despite being created for an early-stage investment pitch.

Nubank raised $2 million in seed funding in July 2013 with this pitch deck. The funding came from Sequoia Capital and Kaszek Ventures. Notably, David Vélez raised this capital without even having formal co-founders in place at the time, demonstrating the persuasive power of his pitch and personal credibility. Nicolas Szekasy from Kaszek famously stated: 'It was David and his PowerPoint, and we invested in the PowerPoint.'

The Nubank pitch deck succeeded through several key elements: (1) identification of an enormous, obvious pain point—banking was 'widely hated' in Brazil; (2) founder credibility and clarity—David Vélez's background in venture capital and intelligent articulation of strategy; (3) clear market opportunity—a massive economy (Latin America's most valuable) with entrenched, inefficient incumbents; (4) balanced approach—combining analytical rigor with emotional narrative; (5) strategic positioning as the 'anti-bank' that would transform consumer banking; and (6) focused execution plan—starting with a single product (credit cards) in a single market (Brazil) before expansion.

While Nubank's pitch deck provides valuable lessons in structure and messaging, it should not be used as a direct template because: (1) it was created for a specific market (Brazil) and problem (banking dissatisfaction) that may not apply to your business; (2) modern pitch decks now include additional elements like detailed financial projections, explicit risk analysis, and traction metrics that Nubank's seed deck minimized; (3) investor expectations have evolved significantly since 2013 with more emphasis on unit economics and go-to-market strategy. Instead, use Nubank's deck as inspiration for narrative structure, positioning clarity, and founder credibility while adapting content to your specific opportunity and market conditions.

Nubank was at the pre-seed to seed stage when they created this pitch deck in 2013. David Vélez raised the $2 million seed round without formal co-founders and with minimal operational proof points—the investment was primarily based on founder credibility and market opportunity. This was exceptionally early-stage funding, as Vélez had not yet even recruited his full founding team. After this seed round, Nubank went on to raise subsequent funding rounds (Series A, B, C, etc.) before eventually going public in December 2021 at a valuation of approximately $30 billion.

Creating an effective pitch deck requires more than following a template — it demands strategic clarity about your value proposition, a deep understanding of your target investors, and rigorous financial modelling to support your narrative. At Projects RH, we combine financial expertise with strategic storytelling to build pitch decks, information memorandums, and financial models that meet the standards of institutional investors worldwide. Our team has generated over USD 2.0 billion in expressions of interest across mining, energy, technology, medtech, and financial services sectors. Schedule a consultation to discuss how we can help position your company for successful capital raising.